As soon as thought of a fleeting fad, cryptocurrency has teetered towards changing into a extra mainstream monetary medium lately, inflicting an growing variety of U.S. banks to discover the decentralized system. However reaping its rewards means embracing an trade rife with volatility and danger — inflicting smaller, native banks to avoid the enterprise altogether.

As of January, the Federal Deposit Insurance coverage Company reported that it was conscious of 136 insured banks that have been concerned in ongoing or deliberate cryptocurrency-related actions, reminiscent of permitting financial institution prospects to purchase and promote cryptocurrency belongings by preparations with third events or offering deposit providers and lending to crypto asset exchanges. Banks may also sponsor debit playing cards that provide crypto asset rewards.

For individuals who have but to be initiated into the multifaceted world of cryptocurrency, it’s outlined broadly as a digital, encrypted medium of trade that differs from conventional types of forex in that its worth will not be managed or maintained by a government. Most cryptocurrencies, together with the 2 hottest, Bitcoin and Ethereum, are constructed on blockchain expertise and are categorized as being “pseudo-anonymous,” that means transactions can’t be simply traced again to a person’s real-world identification.

Bigger establishments can afford to run the dangers of partaking with cryptocurrency, which has soared in recognition because it was first launched in 2009. JPMorgan Chase, for instance, debuted its personal digital forex, JPM Coin, in 2020 and employs one of many largest crypto groups within the banking sector to assist allow prompt switch and clearing of multi-bank, multi-currency belongings on a permissioned distributed ledger, in response to its web site.

This can be a carousel. Use Subsequent and Earlier buttons to navigate

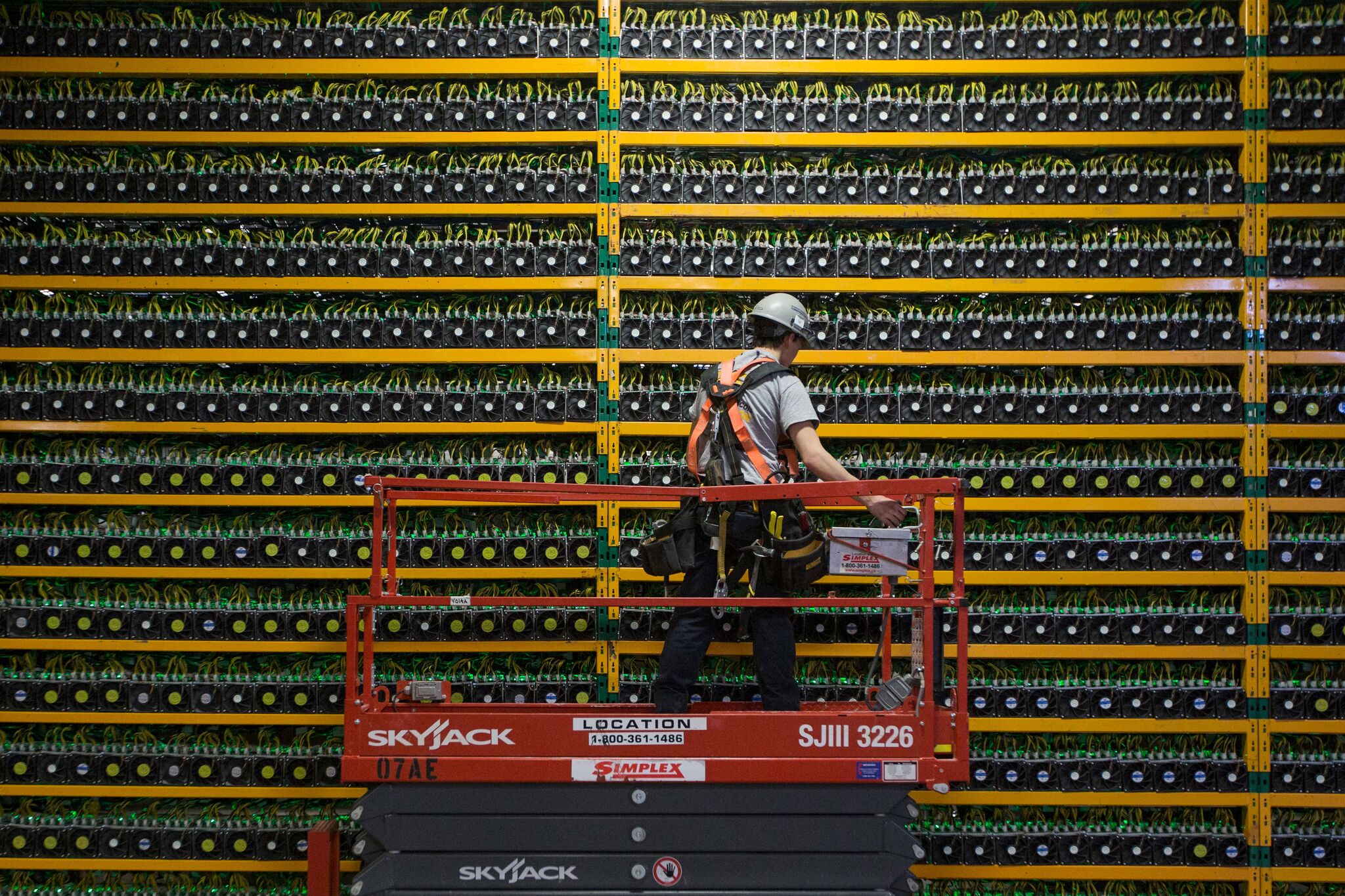

A technician inspects the bottom of bitcoin mining at Bitfarms in Saint Hyacinthe, Quebec. Regardless of its rising recognition, native and regional banks have chosen to avoid cryptocurrency because of the medium’s excessive volatility and related dangers. (Picture by Lars Hagberg /Getty Pictures)

LARS HAGBERG/AFP through Getty Pictures

Not all massive banks have been as fast to leap on board. Financial institution of America doesn’t straight assist the acquisition of cryptocurrencies by its on-line banking platform, though prospects can nonetheless purchase crypto belongings by connecting their accounts to a regulated trade platform.

“There’s clearly lots of inherent danger with the best way these markets are and the way risky they are often and with it not being accepted on a federal degree to make use of as a cost essentially, relying on what you’re doing, it’s one thing that lots of the bigger monetary establishments have no real interest in adopting,” mentioned Dana Martincic, enterprise options advisor at Financial institution of America in Albany. “It sort of goes in opposition to banking; I feel crypto, in actuality, is individuals attempting to avoid banks more often than not they’re utilizing it.”

Most native banks like Trustco, Capital Financial institution, Pioneer Financial institution, Keybank and M&T Financial institution don’t provide any crypto-related providers and as an alternative, rely totally on the extra secure practices of accepting financial savings account deposits and writing residence mortgages.

It’s doubtless that the current turmoil within the monetary sector solely additional solidified their disinterest in getting into the house. Final November, cryptocurrency trade FTX filed for chapter when it ran out of cash after the equal of a financial institution run. The crash rattled the already unstable crypto market, inflicting billions of {dollars} in loss. There have been 11 banks that had been doing enterprise with FTX and will have been concerned in alleged wire switch fraud, in response to a February report from the Workplace of the Inspector Normal.

The Federal Reserve, Federal Deposit Insurance coverage Company and Workplace of the Comptroller of the Forex issued a joint assertion in January advising U.S. banks on the dangers of coping with cryptocurrencies and the significance of stopping crypto-related dangers that can not be mitigated or managed from migrating into the banking system.

“The occasions of the previous 12 months have been marked by vital volatility and the publicity of vulnerabilities within the crypto-asset sector. These occasions spotlight various key dangers related to crypto-assets and crypto-asset sector members that banking organizations ought to pay attention to,” the assertion reads, citing fraud and scams amongst crypto-asset sector members, authorized uncertainties associated to custody practices, redemptions and possession rights and inaccurate or deceptive representations and disclosures by crypto-asset corporations.

Days after the failure of California-based Silicon Valley Financial institution, which despatched shock waves by the economic system, New York Metropolis-based Signature Financial institution was seized by the state Division of Monetary Providers to forestall a subsequent financial institution run. DFS Superintendent Adrienne Harris mentioned whereas cryptocurrency wasn’t Signature’s most important enterprise — the financial institution didn’t have its personal crypto cash, nevertheless it provided a platform for crypto buying and selling — the information that it was concerned with the medium brought about sufficient withdrawals by nervous prospects to get the financial institution on the state regulators’ radar. Some say the regulatory takeover sends a robust message to different banks to avoid crypto belongings or danger dealing with the identical destiny.

However others, particularly fintech professionals and crypto traders, say smaller banks opting out of crypto are lacking out on profitable alternatives for development.

“One factor they need to think about is that these dangers may very well be mitigated by making certain a few of these digital belongings or crypto or monetary merchandise have correct rules and protections for shoppers,” mentioned Nancy Min, founding father of ecoLONG, an Albany-based startup that created a market for renewable vitality buying and selling constructed on blockchain expertise. “The best way that I see blockchain expertise, digital belongings and cryptocurrencies, they maintain lots of potential as a decentralized expertise that makes use of this consensus mechanism to perform a democratic course of and due to this expertise and course of, it permits us to construct belief in an untrusted atmosphere.”

Min rebuffs the declare that cryptocurrencies as a complete threaten the protection of the banking trade and as an alternative, she encourages banks to contemplate providing central financial institution digital currencies, a type of government-issued forex that isn’t backed by a bodily commodity like {dollars}. “I feel that’s the place there’s lots of worth for banks and lots of worth for shoppers,” she mentioned, including that smaller banks have a fair larger alternative for innovation in fintech than bigger establishments.

As one of many first states to manage digital forex companies that deal in cryptocurrencies on-line, the way forward for New York’s crypto trade stays unclear. In November, Gov. Kathy Hochul authorised a moratorium on what’s referred to as “proof-of-work” cryptocurrency mining, a measure that can be in impact for the subsequent two years as state officers research the environmental impacts associated to the method and decide whether or not fossil fuel-based vegetation can be allowed to be introduced again on-line and used to assist energy the extraordinary laptop processing wanted to create the blockchains that cryptocurrency is manufactured from.