Opinion: ‘Forestall protection’ may fit in soccer, however taking part in it protected is not a recreation winner for retirement traders

American soccer coaches are infamous for placing their groups in “stop protection” mode once they’re main close to the top of a recreation and goal to maintain the opposite crew from placing a profitable discipline purpose or landing on the scoreboard.

For instance, a crew would possibly use 5, six and even seven defensive backs to thwart lengthy cross completions.

The tactic typically works. Usually it doesn’t, because the opposing crew completes a fast sequence of modest-yardage performs to win the sport. Cynics say that the one factor a stop protection prevents is your crew profitable the sport.

Loads of trendy funding methods remind me of the prevent-defense — seemingly protected within the quick run however pricey in the long term. For instance, mean-variance evaluation and the Capital Asset Pricing Mannequin (CAPM) each have been justifiably celebrated (certainly, rewarded with Nobel prizes) for his or her elegant arithmetic and compelling insights, together with the worth of portfolio diversification and the significance of correlations amongst asset returns.

But they’re value-agnostic methods that ignore and undermine the insights of worth investing. Even worse, they gauge danger by short-term fluctuations in market costs.

When an organization is privately owned, potential consumers give attention to the identical issues worth traders give attention to with publicly traded companies — the corporate’s property, earnings and money circulate. They gauge danger by the arrogance they’ve of their long-run projections of the corporate’s earnings.

But as soon as an organization turns into publicly traded, too many traders fixate on annual, month-to-month, even day by day fluctuations in market costs.

This misplaced focus not solely distorts the selection of particular person shares, it additionally warps the allocation of investments between shares and bonds, most clearly in 60/40, target-date, and having your age-in-bonds methods.

A 60/40 technique is 60% shares and 40% bonds. A target-date technique selects a goal retirement date and shifts from shares to bonds as that date nears. For instance, I lately obtained a letter from my employer’s retirement plan stating that the plan’s default funding choice is a goal fund that invests 90% in shares and 10% in bonds till the investor is 40 years previous, shifts regularly to 30% equites and 70% fastened earnings over the following 30 years, and stays at 30/70 after that. An age-in-bonds technique is what it feels like: 40% bonds for a 40-year-old, 60% bonds for a 60-year-old, and so forth.

The motivation for every of those methods is to reap the upper returns from shares whereas utilizing bonds to cushion short-term volatility. But damping short-term volatility is like stop protection in soccer — searching for short-run security and sacrificing long-run success.

Contemplate a 50-year-old whose wage greater than covers dwelling bills, who expects to work for a lot of extra years, is incomes substantial earnings from a inventory portfolio, and can obtain Social Safety advantages sooner or later. A 50% bond portfolio is prone to scale back the eventual bequest considerably and makes it extra possible that this individual will outlive his or her wealth. As this individual turns into 60, 70, 80 years previous and switches to 60%, 70%, 80% bonds, the prices can be even larger.

One other instance. Until they’re actually operating out of cash to pay their payments, it doesn’t make sense for 90-year-olds to have portfolios which are 10% invested in shares, which can be transformed to 40%, 50% and even 60% shares once they die and bequeath their portfolios to their kids.

There are some conditions by which a 100% inventory portfolio is genuinely dangerous — it is advisable liquidate your portfolio quickly to purchase a home or pay in your kids’s school bills — however a common 60/40, target-retirement, or age-in-bonds technique is unquestionably a foul thought for a lot of, if not most, individuals.

Let’s see how such methods would have fared traditionally. This previous December, Congress elevated the age at which required minimal distributions (RMDs) should start to 73. It’s prone to go even larger sooner or later as life expectations enhance.

Contemplate in opposition to that backdrop a month-to-month funding in shares and bonds in a retirement fund, starting at age 25 and persevering with for 50 years, till age 75. Assume that the month-to-month funding is initially $100 and grows by 5% yearly.

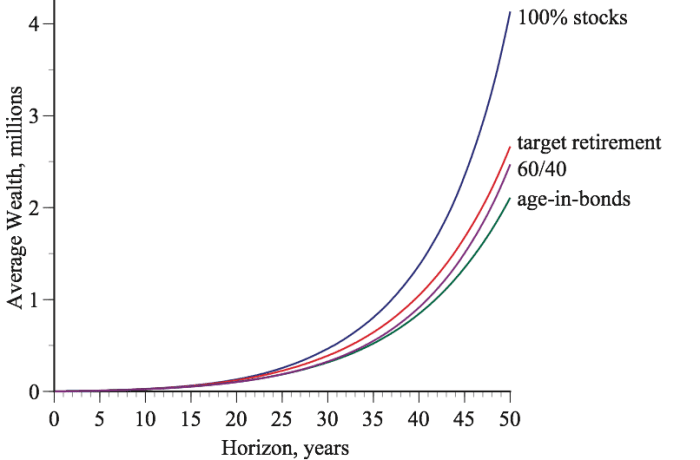

I checked out all attainable beginning dates within the historic knowledge, way back to the info go, to January 1926. The primary determine reveals how usually a 100% inventory technique did higher than three prevent-defense methods for horizons starting from one month to 50 years. Over 30-year horizons, the all-stock technique beat the target-return, age-in-bonds, and 60/40 methods 88%, 92%, and 93% of the time, respectively. Over 50-year horizons, shares gained 93%, 98%, and 99% of the time.

How a lot did this matter? Lots. The determine under reveals the typical wealth over numerous horizons as much as 50 years. The all-stock technique wound up with a median of $4.13 million after 50 years, in comparison with $2.67 million for probably the most profitable prevent-defense technique.

The previous isn’t any assure of the longer term, in fact. Certainly, the entire level of a value-investing perspective is to consider the longer term, not the previous. After I examine shares with bonds presently and searching ahead, shares usually seem like a greater long-run funding — simply as they’ve been up to now.

The present yield on 30-year Treasury bonds

US00,

is round 3.8%, which is an inexpensive estimate of the long-return from bonds except future coupons are reinvested at considerably larger or decrease rates of interest. The present S&P 500

SPX,

dividends-plus-buybacks yield is round 5%. If dividends plus buybacks enhance over time, the long-run return from shares can be even larger — maybe considerably larger. With 5% development within the financial system and company disbursements, the long-run return from shares can be near double digits, because it has been up to now.

For long-term traders who can largely ignore short-term worth volatility, it’s laborious to see how a prevent-defense funding technique is nice for something aside from stopping your monetary victory.

Gary Smith, Fletcher Jones Professor of Economics at Pomona Faculty, is the writer of dozens of analysis articles and 16 books, most lately, Mistrust: Massive Knowledge, Knowledge-Torturing, and the Assault on Science, Oxford College Press, 2023

Extra: Shares gained’t make you massive cash over the following decade, however they’re your finest wager to beat inflation. The guru of index investing explains why.

Additionally learn: Beating the inventory market over time is subsequent to unimaginable, however you must nonetheless attempt.